There is currently no legal definition of ‘crypto-assets’ within EU financial securities laws. The European Securities and Markets Authority (ESMA) therefore undertook, in summer 2018, a survey of National Competent Authorities of Member States (NCAs) to better understand the circumstances in which crypto-assets may qualify as ‘financial instruments’ in the EU.

29 NCAs participated: 27 Member States (all except Poland), Liechtenstein and Norway.

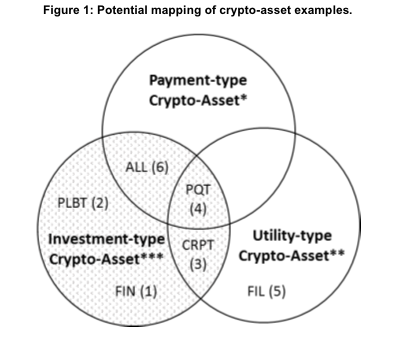

The survey questions aimed to determine (1) the way in which a Member State had transposed MiFID II into national law, and (2) whether a sample set of six ICO crypto-assets qualify as ‘financial instruments’ under the respective national laws.

This sample set of crypto-assets reflected different characteristics:

- Investment-type crypto-assets (cases 1 and 2)

- Utility-type crypto-assets (case 5)

- Hybrids of investment-type, utility-type, and payment-type crypto-assets (cases 3, 4 and 6).

(Pure payment-type crypto-assets, like Bitcoin, are not represented in the sample).

Outcome of the survey:

1. Most NCAs have the view that crypto-assets (cases 1, 2, 4 and 6) could be considered transferable securities and/or other types of financial instruments as defined under MiFID II.

2. The fact that a crypto-asset has profit-rights attached, without necessarily having ownership or governance rights attached (crypto-asset cases 1 and 2), is considered sufficient for a majority of NCAs to qualify the crypto-asset as ‘transferable security’ – whether as shares or as another type of transferable security.

3. No NCAs labelled the crypto-asset case 5 as transferable security or financial instrument, which suggests that pure utility-type crypto-assets may fall outside the existing financial regulations across the Member States. The reason may be that the rights they convey seem to be too far removed from the financial and monetary structure of a transferable security or a financial instrument.

4. The vast majority of NCAs did not believe that any national regulations currently in place would capture any of the six crypto-asset case studies.

5. There is broad agreement among NCAs on the notion that crypto-assets that meet the necessary requirements to qualify as ‘financial instruments’ should be regulated as such.

6. A number of NCAs suggested that there is a need for changes to existing legislation, or additional legal provisions, to respond to the unique characteristics of the crypto-assets sector; these characteristics relate to the decentralised nature of the Blockchain technology, the risk of forks, and the custody of the underlying assets.

7. The vast majority of NCAs considered that the qualification of all crypto-assets as financial instruments would have negative collateral effects. Therefore, there might be a need to distinguish between the different types of crypto-assets, which is understandable given the variety of crypto-assets being issued.

The reasons given for a differentiating legal approach were:

(1) the fact that existing legal regulations were drafted without the awareness of distributed ledger technologies or crypto-assets;

(2) that acknowledging crypto-assets as ‘financial instruments’ would grant them potentially unwanted legitimacy; and

(3) there are insufficient supervisory tools and resources.

Although the vast majority of NCAs agreed that all crypto-assets need to be subject to some kind of legal regulation, diverging views among the NCAs exist on (1) whether these regulations should be within the scope of MiFID or outside of it, and (2) the extent of those regulations.